Trading in Thames Water bonds has rocketed amid mounting concerns over the fate of the UK utility after its parent Kemble Water Finance defaulted on its debt earlier in April.

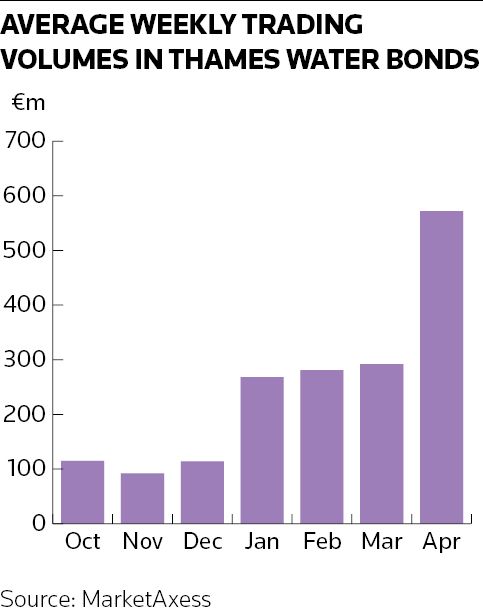

An average of €572m in Thames Water corporate bonds have changed hands each week this month, according to data from trading platform MarketAxess, reaching a peak of €813m in the week to April 14 in the aftermath of Kemble saying it would default on payments to bondholders. That compares to average weekly volumes of €108m in the three months to December 31.

It is common for bond trading volumes to rise sharply when a company runs into difficulties, as institutional investors such as asset managers and pension funds sell to hedge funds and other firms that specialise in distressed debt. Traders said this playbook explains the recent upswing in activity around Thames Water, with reports that Elliott Management has been among the buyers of its debt. The US hedge fund declined to comment.

“There’s been a transition from real-money [investors] into hedge funds or [distressed funds],” said a senior credit trader at a major bank.

But the trader also said there is not an outright sense of panic despite the negative headlines around Thames Water because of the whole business securitisation structure its operating company used to issue its bonds – as well as the liquidity it has on hand.

“I would say that unlike other single-name, high-yield stories, Thames [which at the operating company level is still rated investment grade] still feels relatively insulated in the sense that the big UK insurers, big UK accounts have not necessarily sold, because within that securitisation they still have £2.5bn of [liquidity],” the trader said. “[Water regulator] Ofwat still has a few permutations before we get to a really, really bad case scenario.”

Investors in the bonds of Thames Water's operating company, which comprise £15bn of Class A and £1.3bn of Class B notes, were due to meet last Monday to discuss their options. There are concerns that bondholders may be vulnerable to a writedown on their debt if the beleaguered water company doesn’t receive another injection of equity.

Trouble shorting

Complicating matters for bearish investors is the fact that they don't have one of their favoured tools at their disposal – the credit default swap market – to bet against or hedge Thames Water debt. S&P Global Market Intelligence, which collects and publishes CDS data, said it doesn’t have prices on Thames or Kemble CDS as it doesn’t observe sufficient liquidity in the market.

It’s also not easy to execute another common short-selling strategy: borrowing Thames bonds with the idea of selling them and then buying them back at a lower price. The steep price declines in these securities make them very expensive to borrow, eroding returns that can be made from a drop in prices.

“It’s super expensive [to short],” the trader said. “Some guys have traded in and out and they might have done well, but the timing is very important.”

That dynamic may explain why S&P data show there are only negligible amounts on loan for three Thames Water Class A bonds it tracks that mature in 2028, 2032 and 2040, which are trading at between roughly 60% and 80% of face value, according to LSEG data.

There are more securities out on loan – and therefore probably in the hands of short-sellers – for two other Class A Thames bonds maturing in 2027 and 2028, which trade at closer to 90% of face value and are cheaper to bet against. However, the S&P data show that short interest has fallen lately in these securities too. The amount of the 2027 bond out on loan is now around 11% compared with almost a quarter of the value of those securities earlier this month.